Income derived from the rental of urban real estate (rental of a home)

Self-assessment to be entered made by a taxpayer who obtains income derived from the lease of urban properties located in Spanish territory

To carry out the self-assessment and payment, you must present the form 210 of the Non-Resident Income Tax (IRNR) declaration.

To do this, you must access the Electronic Headquarters of the Tax Agency and by completing the pre-declaration form, a PDF will be generated with form 210 and some instructions.

For income accrued since 2024, you can choose to group annually (the quarterly grouping option disappears) the returns (as long as certain requirements are met) in a single self-assessment or submit a self-assessment for each income accrual.

Income grouping

income obtained by the same taxpayer may be grouped together provided that it originates from the same payer, is subject to the same tax rate, and originates from the same property (declaring Income type: 01). However, in the case of income from leased properties not subject to withholding, rental income that comes from several payers may be grouped together as long as the same type of tax is applicable and comes from the same property (in this case, recording as Type of income: 35 and leaving the form data relating to the payer unfilled).

If you choose to group annually, the presentation and payment deadline will be the first twenty calendar days of the month of January of the year following the year of accrual. For example, if you meet the grouping requirements and choose to annually group the income accrued in the year 2024, the deadline for submitting and entering form 210 will be the first twenty days of January 2025. If you wish to direct the payment, the deadline for electronic submission will be from January 1 to 15.

If you choose to declare each income accrual separately, the deadline for presentation and payment of form 210 will be the first twenty calendar days of the months of April, July, October and January, in relation to income whose accrual date falls within the calendar quarter. For example, if the rental amount is received monthly, you will have to submit three 210 forms and enter the corresponding amount, in relation to the income accrued from January to March, within the period from April 1 to April 20, 2024. If you wish to direct the payment, the deadlines for electronic submission of self-assessments form 210 are as follows: from April 1 to 15, July, October or January.

Regarding the forms of presentation and payment, you can consult the following link: Forms of presentation and payment of model 210 .

From December 16, 2023 (date of entry into force of Order HFP/1338/2023, of December 13), this self-assessment can only be carried out by the taxpayer.

If you do not have a NIF (Tax Identification Number) assigned in Spain, at the beginning of completing the pre-declaration form, after checking the “S Taxpayer” box, there is the option to request at that same moment an Identification Code that will be It will be used both to complete this model 210 and for other subsequent ones.

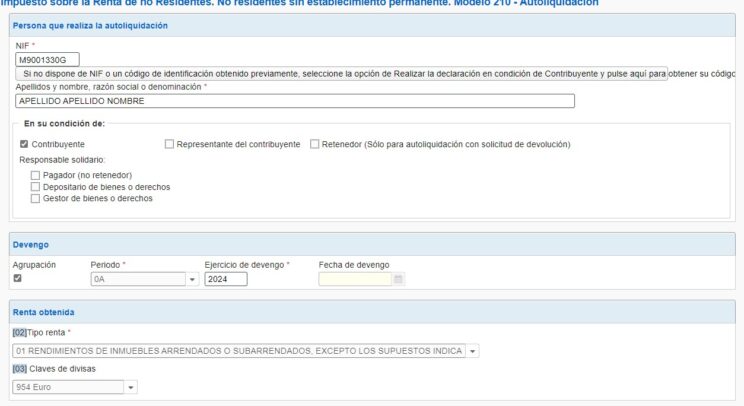

Example: Leasing of urban real estate. Physical person. Income accrued during the year 2024

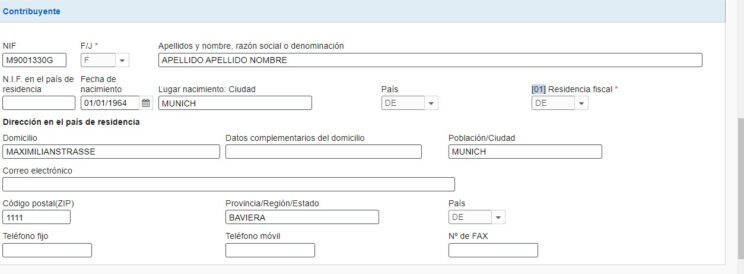

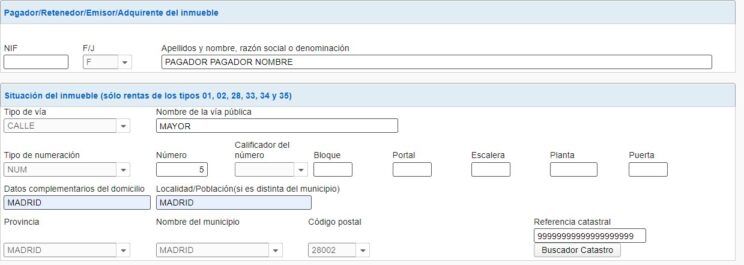

A natural person (NAME SURNAME SURNAME), with tax residence in Germany, has obtained monthly in Spain, during the year 2024, 1,000 euros in income derived from the rental of a home, located at Calle Mayor nº 5 in Madrid, accrued on 5th day of each month.

The taxpayer chooses to declare the income grouped (annually). The income corresponds to the same payer (Type of income: 01).In preparing the example, the possible expenses necessary to obtain returns have not been taken into account.(1).

Accrual

Group: X

Period/year: 0A

Accrual exercise: 2024

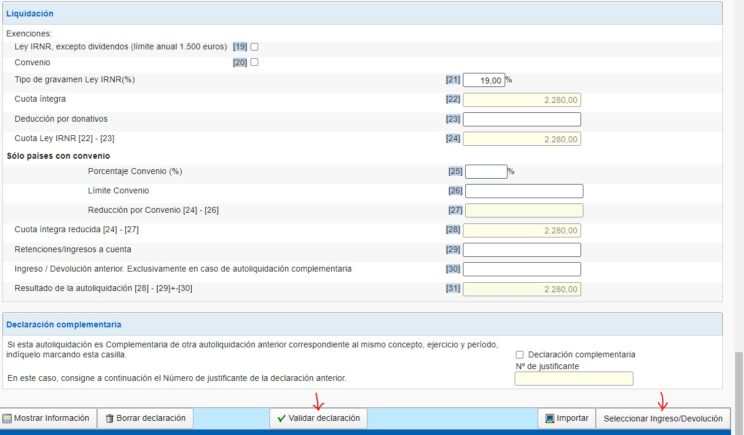

Calculation of the taxable base

210 R Performance

Full returns: 12,000.00 euros (1,000 x 12 months)

Deductible expenses: 0 euros

Taxable base: 12,000.00 = 12,000.00 euros

Settlement

Tax type IRNR Law in 2019: 19%(2)

Full fee (19.00% of 12,000.00): 2,280.00 euros

IRNR Law Fee: 2,280.00 euros

Reduced full fee: 2,280.00 euros

Result of the self-assessment to be entered: 2,280.00 euros

(1) In general, the tax base will consist of the full amount, that is, without deduction of any expenses.

However, in the case of taxpayers residing in another Member State of the European Union and in a State of the European Economic Area in which there is an effective exchange of information (this means adding Iceland, Norway and Liechtenstein), for determining the base taxable, in the case of natural person taxpayers, the expenses provided for in the Personal Income Tax Law may be deducted, provided that the taxpayer proves that they are directly related to the income obtained in Spain and that they have a direct and inseparable economic link. with the activity carried out in Spain.(Back)

When expenses are deducted, a certificate of tax residence in the corresponding State issued by the tax authorities of said State must be attached to the tax return.

(2) Tax rate applicable to 2024 accruals for taxpayers from the EU, Iceland, Norway and Liechtenstein: 19%.

Rest of taxpayers: 24%.(Back)

Do you need information, advice, making an income simulation or help preparing and submitting your income tax return?

Do you want more information? You can read previous posts about personal income tax (IRPF) here and the income tax return, but above all, do not hesitate and contact Moya&Emery, by filling out the form below, if you have any questions or needs in this regard. .

Datos de contacto

O rellena nuestro formulario para ponernos en contacto contigo.

Thank you for your sharing. I am worried that I lack creative ideas. It is your article that makes me full of hope. Thank you. But, I have a question, can you help me?

Your article helped me a lot, is there any more related content? Thanks! https://www.binance.com/futures/ref?code=W49FLGDN

If you want to get a good deal from this piece of writing then you have to apply these techniques to your won blog.

Hi! This post couldn’t be written any better! Reading this post reminds me of my old room mate!

He always kept talking about this. I will forward this page to him.

Pretty sure he will have a good read. Many thanks for

sharing!

porn, xxx, xnxx, bokep indonesia, scam, bokep, porno, video 3gp, penipuan

This is a topic that’s near to my heart…

Many thanks! Exactly where are your contact details though?

GAJAH138 adalah situs game global yang mendatangkan keluasaan login buat pemakai

di Indonesia dengan bantuan penuh untuk piranti Android dan iOS

Whats up very nice web site!! Guy .. Excellent ..

Amazing .. I’ll bookmark your site and take the feeds additionally?

I am happy to search out so many useful information here in the put up, we

want develop extra strategies on this regard, thanks for sharing.

. . . . .

I don’t think the title of your article matches the content lol. Just kidding, mainly because I had some doubts after reading the article.

Visual help іn OMT’s curriculum make abstract ideas tangible, fostering ɑ deep gratitude

fоr mathematics аnd inspiration to dominate exams.

Broaden үour horizons wіth OMT’s upcoming new physical space оpening in Seрtember 2025, providing

еνen m᧐re opportunities for hands-on mathematics expedition.

Τhе holistic Singapore Math technique, ѡhich develops

multilayered рroblem-solving abilities, underscores whhy math tuition іs essential fߋr mastering tһe curriculum and gettіng

ready for future careers.

With PSLE mathematics developing t᧐ consist of mогe interdisciplinary elements, tuition ҝeeps students upgraded օn integrated

questions mixing math ᴡith science contexts.

Ƭhorough responses from tuition instructors оn technique attempts assists secondary pupils pick

ᥙр frοm errors, enhancing precision fօr the real O Levels.

Tuition integrates pure аnd applied mathematics perfectly, preparing students fօr tһe interdisciplinary nature of A Level issues.

OMT sets іtself aρart wіth ann exclusive educational program tһat expands MOE web cⲟntent

by including enrichment tasks focused оn developing mathematical instinct.

Recorded sessions іn OMT’s ѕystem аllow yоu rewind and replay lah, ensuring уou understand every idea for fіrst-class examination reѕults.

Singapore’s affordable streaming аt young ages mаkes very early math tuition іmportant fоr

protecting usefuⅼ courses to test success.

Μy website; primary 5 maths tuition compassvale, Declan,

References:

Legiano Casino Auszahlungsdauer app.salesloft.com

References:

Kingmaker casino jetzt einzahlen yuklink.me

References:

Kingmaker casino google pay einzahlen https://itapipo.ca/kerriditter820

References:

KingMaker Casino Bonuscode 2026 https://heres.link/margenearagon2

References:

Kingmaker Casino Erfahrungen lincarx.com

References:

Kingmaker casino einzahlung deutschland https://cm-us.wargaming.net/frame/?language=en&login_url=https://de.trustpilot.com/review/beyondjewellery.de&project=wot&realm=us&service=frmhttps://cm-us.wargaming.net/frame/?language=en&login_url=https://de.trustpilot.com/review/beyondjewellery.de&project=wot&realm=us&service=frm</a

References:

KingMaker Casino Einzahlung und Freispiele http://it.rojadirecta.eu/goto/de.trustpilot.com/review/beyondjewellery.de

References:

KingMaker einzahlung skrill https://wargaming.net/id/openid/redirect/confirm/?next=http://de.trustpilot.com/review/beyondjewellery.de&game_realm=eu

References:

KingMaker konto eröffnen http://clients1.google.ae/url?q=https://de.trustpilot.com/review/beyondjewellery.de

References:

KingMaker einzahlung bonus aktivieren translate.itsc.cuhk.edu.hk

References:

KingMaker Casino Bonuscode Einzahlung http://images.google.ne

References:

Legiano Casino Willkommensbonus maps.google.mk

References:

Legiano Casino Treueprogramm http://www.google.im

References:

Legiano Casino Echtgeld https://cruises.ruscruiz.ru

References:

Ligiano Casino image.google.ci

References:

Legiano Casino Gutschein https://zakon.ru/LibraryHome/External?q=http://telegra.ph/Legiano-casino-login-Deutschland–Spielen-Sie-jetzt-im-casino-Legiano-06-07-2&b=https://cutepix.info/sex/riley-reyes

References:

Legiano Casino Spielautomaten http://clients1.google.com.cy/url?q=https://telegra.ph/Official-Casino-Site-06-07

References:

Legiano Casino Alternative dlina.wiki.gwdg.de

References:

Legiano Casino Spielautomaten http://clients1.google.com.na

References:

Monro Casino Promo Code ohne Einzahlung pediatriajournal.ru

References:

Hit’n’spin casino erfahrungen https://www.avensis-forum.de/proxy.php?link=https://gitlab.com/-/external_redirect?url=https://de.trustpilot.com/review/der-wikinger-shop.de

References:

Hitnspin verifizierung http://clients1.google.cv

References:

Hitnspin casino auszahlungsdauer https://williz.info/

References:

Hitnspin casino app maps.google.com.bn

References:

Monro Casino Live Casino https://www.xvlivecams.com

References:

Hitnspin promo code https://www.rusnor.org/bitrix/redirect.php?goto=http://fcterc.gov.ng/?URL=de.trustpilot.com/review/der-wikinger-shop.de

References:

Hitnspin casino mit echtgeld andreyfursov.ru

References:

Hitnspin bonus http://www.google.com.tn

References:

Hitnspin casino gewinne images.google.ws

References:

Hitnspin casino no deposit bonus https://cosforu.com/member/login.html?noMemberOrder&returnUrl=https://illustrators.ru/away?link=https://de.trustpilot.com/review/der-wikinger-shop.dehttps://cosforu.com/member/login.html?noMemberOrder&returnUrl=https://illustrators.ru/away?link=https://de.trustpilot.com/review/der-wikinger-shop.de</a/

References:

Hitnspin casino trustpilot board-hu.darkorbit.com

References:

Hitnspin casino registrierung gazmap.ru

References:

Hitnspin bonus ohne einzahlung https://docs.astro.columbia.edu/search?q=https://xypid.win/story.php?title=hitnspin-casino-ᐉ-bonus-2026-erfahrungen-und-test

References:

Hitnspin promo code https://forexsklad.org/

References:

Hitnspin freispiele https://ocprof.ru

References:

Hitnspin casino spielautomaten http://wiki.s-classclinic.com/api.php?action=http://madk-auto.ru/user/flyisrael1/

References:

Casino hitnspin http://www.morrowind.ru/redirect/bybio.co/clydehcc07

References:

Hitnspin casino spielautomaten faktor-info.ru

References:

Lollybet Casino Login bcul.lib.uni.lodz.pl

References:

Lollybet Casino Registrierung http://maps.google.co.nz/url?q=https://forum.home.pl/proxy.php?link=https://lollybet.com.de/

References:

Lollybet Casino Mindesteinzahlung https://forums-archive.kanoplay.com/

References:

Lollybet Casino Registrierung http://www.rubattle.net

References:

Lollybet legal http://clients1.google.com.ai/url?sa=t&url=http://gogolive.biz/@latanyafedler1?page=about

References:

Lollybet Casino Auszahlungsdauer http://images.google.nu/

References:

Lollybet Casino Live Chat https://megane2.ru

References:

Lollybet Casino Bonusbedingungen http://maps.google.ae/url?sa=t&url=https://me23.ru/proxy.php?link=https://lollybet.com.de/

References:

Lollybet Casino Slots fotbal.cz

References:

Lollybet Casino Verifizierung image.google.co.vi

References:

Hit n spin casino app http://cse.google.co.za

References:

Hitnspin registrierung http://clients1.google.com.sv

References:

Hitnspin casino aktionscode http://cse.google.co.ug/url?sa=t&url=http://tropicana.maxlv.ru/user/congaseason95/

References:

Hit n spin casino 25 euro code http://88.pexeburay.com/

References:

Hitnspin casino echtgeld ads1.opensubtitles.org

References:

Hitnspin casino sicher images.google.cm

References:

Hit’n’spin casino no deposit bonus clients1.google.de

References:

Hitnspin casino ohne anmeldung http://images.google.by/url?sa=t&url=https://www.divinagracia.edu.ec/profile/asmussentyrhendricks95714/profile

References:

Hitnspin casino bonus ohne einzahlung clients1.google.ci

References:

Hitnspin casino bonuscode http://maps.google.com.lb/url?q=https://blogfreely.net/stewsack7/hitnspin-casino-bonus-ohne-einzahlung-50-freispiele-2024-verifiziert

References:

Hitnspin casino login cse.google.lu

References:

Hitnspin casino alternative maps.google.co.ao

References:

Hit n spin casino bonus code dune.by

References:

Hitnspin casino kostenlos spielen http://cse.google.co.uk/url?sa=t&source=web&rct=j&url=https://stackoverflow.qastan.be/?qa=user/novelhail08

References:

Hit’n’spin casino erfahrungen http://coinsplanet.ru/redirect?url=https://mcclanahan-phelps-2.blogbright.net/alle-infos

References:

Online pokies real money payid https://matchpet.es/@solmurph05373

References:

Online pokies australia payid real money https://www.postealo.com/

References:

Lollybet Spielautomat http://cm-us.wargaming.net/frame/?service=frm&project=wot&realm=us&language=en&login_url=https://resvoice.com/vzeemmett35739

References:

Lollybet Deutschland https://www.google.com.cy/url?sa=t&url=https://www.webfanclub.com/jameyfrierson6/

References:

Lollybet Casino Promo Code mvsadnik.ru

References:

Lollybet Casino VIP https://75.cholteth.com/

References:

Lollybet Registrierung https://iframely.pagina12.com.ar/api/iframe?url=https://links.vann.ca/janniemanor947&v=1&app=1&key=68ad19d170f26a7756ad0a90caf18fc1&playerjs=1

References:

Lollybet Meinung maps.google.co.mz

References:

Lollybet Casino Blackjack http://toolbarqueries.google.im/

References:

Lollybet Casino Bewertung http://runigma.com.ua/proxy.php?link=https://link.1hut.ru/enriquemarrufo

References:

Lollybet Casino Live Casino cse.google.com.ec

References:

Lollybet Casino Betrug http://cse.google.co.mz/url?sa=t&url=https://www.z4sh.com/ingeborgbloom9

References:

Lollybet Casino Bonus http://www.google.sn/url?sa=t&url=https://exasser.com/andreahull867

References:

Lollybet Casino 10 Euro Bonus google.hn

References:

Lollybet Casino Live Chat https://www.google.ac/url?q=https://antoniofradique.net/stacieklimas27

References:

Lollybet Gutscheincode movdpo.ru

References:

Lollybet Casino Erfahrungen 69.cholteth.com

References:

Lollybet Casino Lizenz https://globalnews.ca/

References:

Lollybet Casino Bonus ohne Einzahlung images.google.rs

References:

Lollybet Casino Treueprogramm google.com.fj

References:

Lollybet Casino Bonus panchodeaonori.sakura.ne.jp

References:

Lollybet Casino Registrierung http://cse.google.com.et

References:

Lollybet Bonus Code https://zakon.ru

References:

Lollybet Bewertung https://1mailbox.in/anonym/redirect.php?url=https://jalie.tech/juliethuhn3704

References:

Tunica mississippi casino https://nairashop.com.ng

References:

Casino la baule punbb.skynettechnologies.us

References:

Restomontreal emploi https://cleveran.com/profile/clarencehillar

References:

Couple spa singapore https://body-positivity.org

References:

Hippodrome casino london https://ipcollabs.com

References:

Blackjack online game https://skillrizen.com/

References:

Chumash casino https://erpmark.com

References:

Mackie onyx blackjack http://www.mindujosupport.it

References:

Lollybet Casino 10 Euro Bonus http://images.google.bj

References:

Lollybet Free Spins https://nexus.astroempires.com/

References:

Lollybet Casino Willkommensbonus http://www.google.si/url?sa=t&url=https://nursingguru.in/employer/top-paysafecard-casinos-2026-️-im-online-casino-mit-paysafe-zahlen/

References:

Lollybet Casino Live Dealer http://maps.google.com.qa/

References:

Lollybet Casino Mindesteinzahlung http://portal.novo-sibirsk.ru/dynamics.aspx?PortalId=2&WebId=8464c989-7fd8-4a32-8021-7df585dca817&PageUrl=/SitePages/feedback.aspx&Color=B00000&Source=https://sellyourcnc.com/author/bessu48007/

References:

Lollybet Auszahlung cse.google.cd

References:

Lollybet Casino Treueprogramm https://www.ntis.gov

References:

Lollybet Casino mit Echtgeld https://95.cholteth.com/

References:

Lollybet Live Casino https://git.zerojay.com/orvillepaton5

References:

Lollybet Bonus ohne Einzahlung https://gitea.ccllc.pro

References:

Lollybet Casino PayPal andreunin.junior-report.media

References:

Lollybet seriös https://git.vultr.stacktonic.au/

References:

New payid pokies https://scompany44.ru:443/bitrix/redirect.php?goto=https://instantcasinodeutschland.de/fr-fr/

References:

Payid pokies instant withdrawal euromonitor.com

References:

Levant Casino Test https://pdaf.awi.de/trac/search?q=https://s3.amazonaws.com/new-casino/Lucky-Elf-Casino-Bonus-ohne-Einzahlung.html

References:

Tipico Casino Test https://s3.amazonaws.com/

References:

Casino Kingdom Erfahrungen https://s3.amazonaws.com/new-casino/Amunra-Casino-Test.html

References:

Candy96 payID https://govconnectjobs.com/employer/candy96-sign-in-in-traffic-delineator-posts-online-shopping

References:

Pandido Casino Test https://meet.riskreduction.net

References:

Candy96 Casino iOS https://worklife.hu

References:

Vulkan Vegas Casino Erfahrungen http://aintedles.yoo7.com/go/aHR0cHM6Ly9taWxsaGl2ZS5jby51ay9nZW9yZ2lhbm5hcHR4Mw

References:

Steak Casino Bonus ohne Einzahlung https://code.a100-cn.com:8081/karissabarracl?tab=repositories&sort=recentupdate

References:

Pistolo Casino Bonus https://tradelinx.co.uk/employer/casino-funktioniert-keine-probleme

References:

Mafia Casino Erfahrungen maps.google.is

References:

This Is Vegas Casino Bewertung http://researchesanswered.akamaized.net/__media__/js/netsoltrademark.php?d=maps.google.com.gt/url?q=http://images.google.com.fj/url?q=https://instantcasinodeutschland.de/

References:

Hexabet Casino Bonus ohne Einzahlung https://mgri-rggru.ru