Pension plans for the self-employed

Pension plans for the self-employed. Occupational pension plans In 2023, a new regulation of occupational pension plans has come into force, which has brought with […]

Pension plans for the self-employed. Occupational pension plans In 2023, a new regulation of occupational pension plans has come into force, which has brought with […]

Special tax regime applicable to workers/professionals/entrepreneurs/investors posted to Spanish territory. IMPATRIATES Individuals who acquire their tax residence in Spain because of their displacement to Spanish […]

With the entry into force on January 1, 2023 of Royal Decree-Law 13/2022 of July 26, 2022, a new contribution system is established for self-employed […]

The Minister of Hacienda and Public Function, María Jesús Montero, presented this Thursday the package of tax measures that allow progress towards a fairer tax […]

On 27 July, the Council of Ministers approved the new contribution system for the self-employed. The new system will be based on the net income […]

Taking advantage of deductions continues to be the main weapon of taxpayers to pay less to the Treasury together with good tax planning of their […]

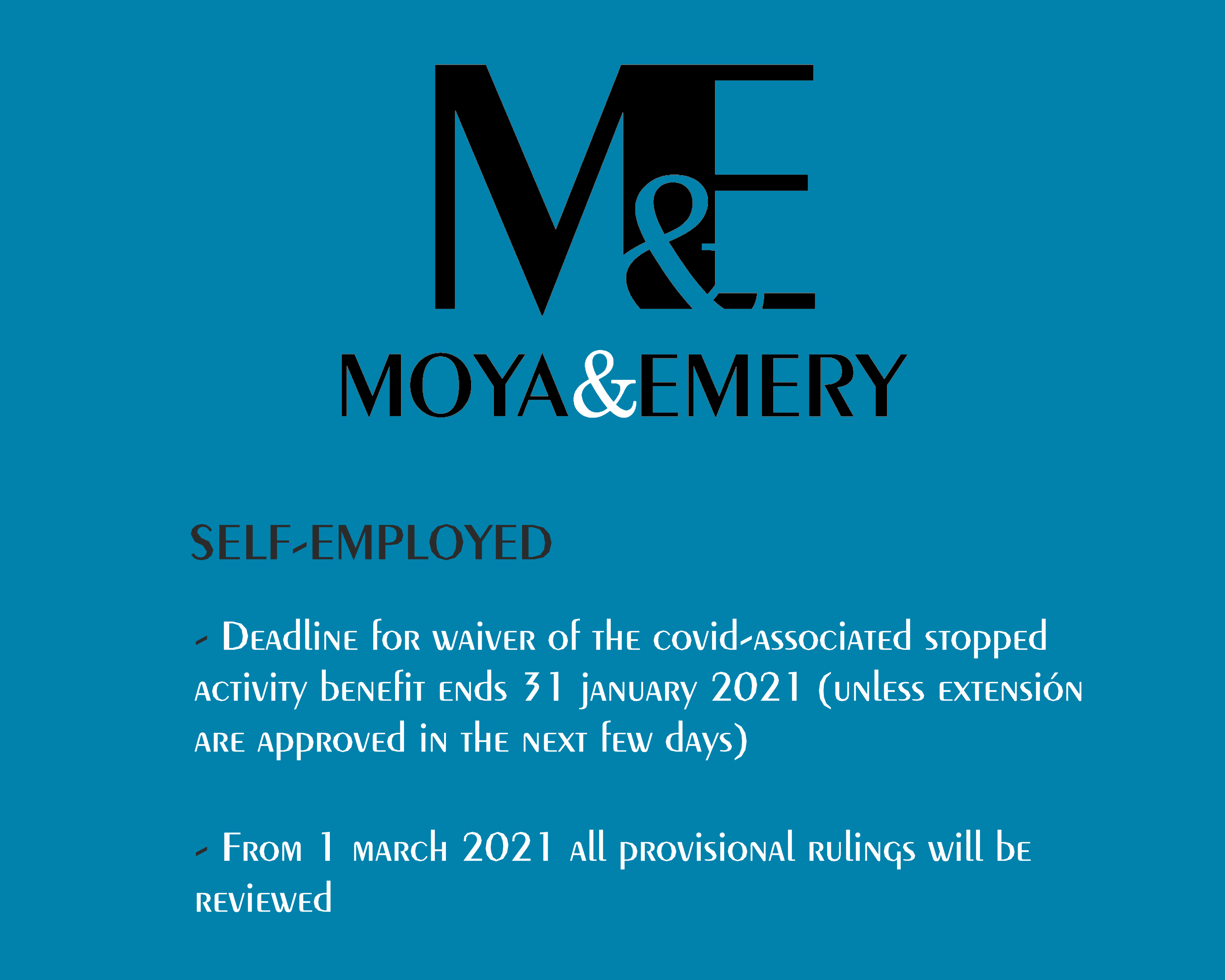

Self-employed. Deadline for waiver of the covid-associated stopped activity benefit ends 31 January 2021 (unless extensión are approved in the next few days)